I find Corporate Venture Capital (CVC) fascinating. For years startups have tried to get Corporates to invest in their ideas. Organizations, though, have been ignoring startups at any turn. Meanwhile, disruptive innovations coming out of them have been shaping the business landscape.

While markets are booming, many corporations allow themselves to ignore the new reality. However, when such disruptions start eroding their market share, they began to turn towards startups for help.

And this is how Corporate Venture Capital (CVC) started and why it’s been growing like mad in the last few years. The number of industries new technology is disrupting is growing exponentially. It’s now hard to find a single vertical that’s not affected. Hence so many organizations looking for novel angles.

The type of growth of such corporate investment, though, is baffling. While pure Corporate Venture Capital (CVC) is growing, investments off balance sheet are going through the roof.

For the sake of clarity, CVC is the investment unit in a corporation that works with a fixed budget or fund. There are many types of CVC; some internal, others external; some with the corporation as single Limited Partner (LP), others with a combination. Nonetheless, investment isn’t always funneled through the CVC, but directly from the balance sheet of the organization.

Many companies are setting their own flavor of CVC. The latest CBInsight report puts the approximate number of them at 733 worldwide. The striking fact though is that direct investments are orders of magnitude bigger than operations through CVC.

Why is Direct Corporate Investment Growing?

That’s precisely what I asked myself. In my head, the growth of CVC makes all the sense, but having direct investments surpassing them by several orders of magnitude is strange. Or is it?

With a little digging and understanding, a clearer picture emerges. Corporate Venture Capital’s goals differ from the purely financial motif that’s the hallmark of traditional VC. It’s not that they aren’t looking for a financial return. However, their motivation is more strategic and combines several aspects.

A big part of investing in startups is to learn from them. It’s not only about the technology or how they use it. It’s also not just about market intelligence. Typically, it’s about connecting people from both worlds to see if any rubs off.

Organizations are desperate for better, faster, stronger innovations for their core business. Their innovation teams aren’t enough, hence the need to adopt open innovation paradigms.

Here is the catch. They’re looking for sustained innovations, not disruption. They want to find startups they can cannibalize, using the new mojo to surpass the competition. As stagnant industries get disrupted, the heat rises and the need for faster leapfrog increases.

Startup Investment Evolution

The first move for newly disrupted companies is to “partner” up with startups. Many organizations realized soon enough that startups aren’t interested in playing ball with them. For young entrepreneurs, integrating and working for a slow, cranky and legacy machine, isn’t the dream. The best startups will pass on partnering, and so Corporations will struggle to attract smart teams to their cause.

The Aleph Report

The second iteration is to invest in them instead. If you can’t partner, let’s buy a piece and make them play. The first direct investments tend to be a disaster. The organization, lacking the procedures, knowledge, language, and strategy to deal with a fast-moving startup, is prompt to asphyxiate the investment.

The natural evolution is to create a specialized group to deal with these investments. The organization will deploy a team in charge of the scouting and relationships with potential investees. This is what we now know as the Corporate Venture Capital (CVC) arm of the company.

Except for some exceptional CVCs, most of them encounter friction between the Corporation and their investment strategy. The added layer between the CVC and the organization hinders the swift adoption of the startup advantage. In other cases, senior executives question the usefulness of some of the portfolio startups. Many see the CVC’s investments as tangential to their interests within the company.

Most organizations live in such limbo. They have open innovation programs that connect with startups and a professional investment branch with flashy investees. However, the effect isn’t felt in the business. The company keeps losing market share at a rapid speed.

This is the point where the need for innovation starts to permeate, not only the innovation department but every single group within the organization.

And it’s at this moment that startup investments start happening in parallel to the CVC. The need for quick incremental innovations is so acute that each department scouts and pushes for their picks.

These startups tend to fulfill specific needs each team has. In most occasions, they fit as optimizations or significant improvements of processes or products the company already has in place.

Some organizations end up killing their CVCs. In other cases, the Corporate Venture Capital becomes a specialized unit that invests in future business models and disruptive technology. Good examples are Intel Capital, Google Ventures or Qualcomm Ventures.

The bottom line: The increased pressure most businesses are under is pushing for a company-wide struggle to invest in anything that can help them retain their market share. Hence why, while CVC investment is growing, direct Corporate investment is three times bigger and more common. It’s also important to keep in mind that CVC is very loosely defined, so the boundary here is still pretty muddy.

Trends that are Shaping Corporate Investment

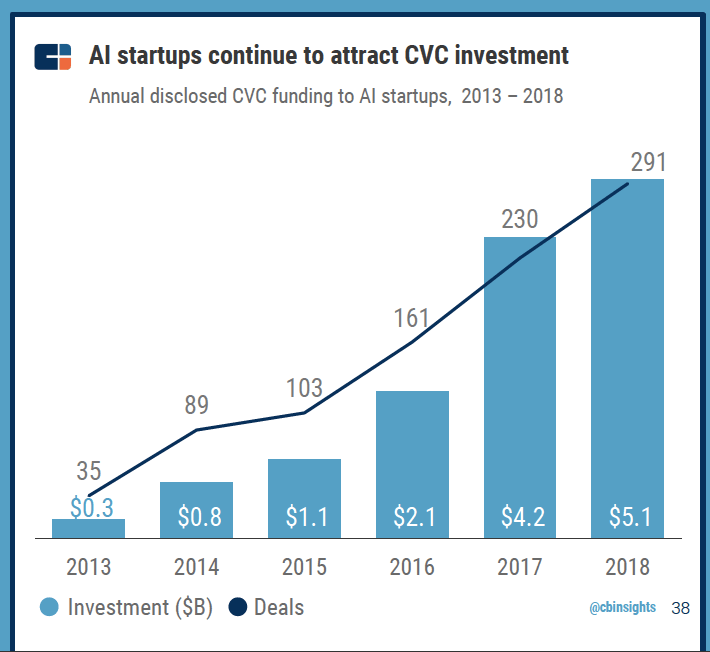

Part of the direct investment we’re seeing is triggered by a major need for most industries, automation. It’s not surprising that Artificial Investments (AI) by CVC is growing exponentially.

Why it matters: Artificial Intelligence (AI) is a very generic term. Under its umbrella, we can fit plenty of different automation tools. Corporations are scrambling to optimize many of their processes, which is one of the reasons for the uptick in AI investments. Precisely because many of these automation startups fit well into many current products, investments are coming off the balance sheet, instead of through the CVC. The larger and more spread out the pain is, the higher the probability the organization will invest directly in it.

The same is true for Cybersecurity. Most of the computational infrastructure has been moving to the cloud for years. With the explosion of connected devices (aka Internet of Things), the computational surfaces of many organizations are multiplying.

Cybersecurity has become critical, not so much as a way to prevent information hacking, but as a safeguard against service disruption.

Many Corporations, sensing (and suffering) the vulnerability of their infrastructure, are investing heavily in proactive measures to maintain the lights on. The truth is, automation is a double-edged blade. It can help optimize an organization, but it also exposes it to very sophisticated and large-scale attacks. As 5G spreads out, the risk of service disruption will grow exponentially.

Be Smart: Companies that invest in Cybersecurity will ensure a double win. On one side they can use the technology to defend themselves. On the other, they can resell these services to less careful competitors and diversify their business.

Next Steps

As we move forward into new disruptive scenarios, incremental innovation won’t be enough. In some industries like the automotive one, it’s already clear as day.

While most investments will still come off the balance sheet, specialized CVC will become critical. The organization will spin them out, so they have real independence. This way they can focus on completely different business models than the mothership.

It’s essential to keep CVC accountable and grounded. Still, many organizations need to learn how to differentiate their business’ KPIs from disruptive ones. Incremental innovation metrics can’t compare to disruptive ones by their very nature. Hence, it’s critical to invest as early as possible in disruptive CVC. It will take time to get it right at first, and many new business model evolutions will need of years to unfold. The moment for structuring an elite disruptive investment unit is now.

If you like this article, please share it, and invite others to follow the newsletter, it really helps us grow!